Hello, this is Yamapan.

I would like to introduce my investment strategy or rather my asset management style.

I also interspersed some of the things I often talk about asset management with other people. I would be happy if people who don't invest read this.

I would be happy if I could get people to invest other than savings accounts even a little after reading this.

Recently, this genre of information has been hot due to the NISA system being reviewed.

I sometimes write about investment or asset management topics on Twitter, but I regularly delete my tweets, so I'm going to blog about it.

I would like to write more, but it would be too long, so I've broken it up.

If you still think it's too long, please take a look at the Recommended Investment Literature at the end.

I think this article will be useful for those who are scared of investing, though it is lukewarm for those who are serious about investing.

I also invest in real estate, which I dare not mention in this article.

There was a time when I did high-leverage FX (888x) and day trading of stocks using margin trading, but I rarely do it now.

I have made close to 1 million in profits and losses in one day, but I can't win consistently right away, and most importantly, day trading bothers me while I'm at work.

Considering my annual income and assets, I thought it would be more important to increase my ability to deposit money first, "in other words, increasing my salary is more important," so I weighed whether I should work or trade during the day and decided that I should work.

So (and for other reasons as well), I basically invest mainly in mutual funds (index investments).

I don't take advantage of special benefits because it is difficult to gather funds from overseas. I think it's OK to invest in dividends, but it's not my main focus at the moment.

Quote from [Stock Investment Notebook] in "Recommended Investment Literature".

- Index investing using mutual funds and leaving it alone is OK.

Contents

Why invest?

There are many different answers.

What does it mean not to invest in the first place before writing a conclusion?

Sometimes people say, "I'm too scared to invest, so I don't do anything.

I'm afraid to invest anything because I'm too scared to invest.

That is actually investing in Japanese yen.

- "Depositing money in the bank" means investing in "Japanese Yen".

To begin with, the value of money today is relative and constantly changing. The value of money changes, and the value of goods also changes.

Specifically, the exchange rate changes every second of every day, and I am sure you have heard that one million yen in the past was worth 30 million in today's terms.

Also, a can of juice that used to cost 100 yen is now 130 yen.

In the case of the recent depreciation of the yen and canned juice, we can consider that the value of the Japanese yen is decreasing.

In other words, if your salary is not increasing, the value of your salary is effectively decreasing.

By the way, it is normal for foreign companies and the like to increase their salaries every year, taking into account the rate of inflation. Recently, Suntory HD raised wages by 6% among Japanese-affiliated companies, which I believe is due to inflation.

Suntory HD is considering a "6% wage increase" including a "bear" wage increase in next year's spring labor offensive in response to an unprecedented rise in prices"](https://news.yahoo.co.jp/articles/a88518632220acdb4aa 37d117fb21890e216efb9)

In such a case, is it really a good idea (high expectation) to invest in Japanese yen? I do not think so.

I think it is better to invest in assets with high expected value.

Difference between stock investment and gambling

Simply put, gambling is a zero-sum game, while stock investment (mutual funds) is not. In other words, there can be a win-win situation for everyone.

In other words, the wealth of the world is not constant, but it is increasing (possibly) due to corporate activities.

Japan is no longer a wealthy country.

Globalization has long been a topic of discussion, but one aspect of globalization is that Japanese people will have to compete with foreign talent.

While the economies of the United States, China, and other developing Asian countries are growing, Japan's economy is not growing or is growing at a relatively slow pace.

In addition, Japan's demographic dividend has ended, and the country is now in a demographic "O" phase, with an inverted pyramid population distribution, which is expected to continue in the future. There are some proposals such as accepting immigrants, but there are concerns and problems with such proposals. Also, even if we want to earn foreign currency, Japanese people cannot speak English (many of them do not), which is also a hurdle.

Under these circumstances, I believe that the value of the Japanese yen will inevitably decline in relative terms.

Suppose I live in such a situation in Japan, and I actually live in Japan.

In that situation, even if you do the same hard work as your parents' generation, you can only live below your parents' generation.

This is a famous Youtube, but you might want to have a look at the following youtube.

https://youtu.be/2DTyHAHaNMw?t=380

All Country Expected Returns and Simulations

The specific stocks are described below, but for the reasons mentioned above and others, I invest mainly in mutual funds that focus on U.S. stocks (All Country has the highest percentage).

Expected Returns

The average yield over the past few decades has been 6-7%.

Of course, there are some years when it is negative, but if you hold for a long period of time, it is generally around this figure.

What is the average yield on global stocks? (if invested for 20 or 30 years)

https://teiiyone.com/blog/2020/12/2030.html

In addition, since the yield of stock investment is compounded, for the same yield, the investment profit will increase year after year after year. In other words, the earlier you start, the better.

- With compound interest, the return on your investment increases every year, so your investment profit will increase every year. This is why it is said that time is your friend. The so-called snowball effect.

Assuming a principal of 1,000,000 yen, no accumulation, and an increase of 10% per year

1st year: 1 million yen + 1 million × 0.1 (100,000 increase)

2nd year: 1,100,000 + 1,100,000 × 0.1 (110,000 increase)

Year 3: 1.21 million + 1.21 million × 0.1 (121,000 increase)

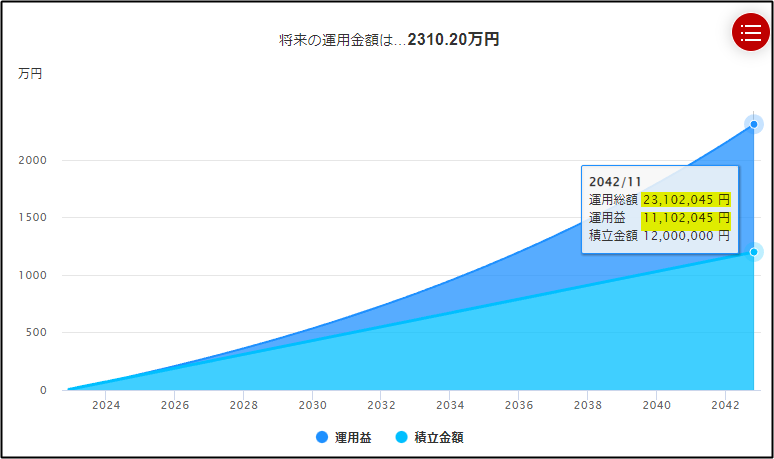

Simulation

Let's look at a more specific simulation.

This is a simulation of a monthly savings of 50,000 yen, yielding 5%, invested for 20 years.

You can see that the amount has doubled in 20 years.

As you can see, the longer you do it, the more your assets will increase.

The simulation can be easily performed at the following Rakuten Securities website.

Easy Simulation of Accumulation

https://www.rakuten-sec.co.jp/web/fund/smartphone/saving/simulation/

Brokerage firm

Basically, it is better to set up with online securities companies because of their low commissions. (We do not recommend major securities companies or banks with salesmen.)

Then, based on the number of stocks they handle, the main ones would be SBI Securities or Rakuten Securities.

(There are also Matsui Securities, Neomova Securities, LINE Securities, GMO Click Securities, etc., but I have not compared them in detail.)

I use SBI Securities by process of elimination because Rakuten is not for me due to religious reasons, but if you are in the Rakuten economy, I think you can get a better deal using Rakuten Securities.

- I prefer online brokerage firms. If you are not particular, SBI Securities or Rakuten Securities are the cheapest.

Specific investment methods (N-1: Pattern of a 30-year-old single male)

The following are the investments that I routinely make in my salary.

Fixed amount reserve investment

I accumulate a fixed amount every month.

Currently, 150,000 yen is debited on my payday every month and set aside for purchases. (This includes 33,000 in savings NISA.)

I review it when I get a raise, change jobs, or have a rollover, but basically I review it once a year.

Once I raise my salary, it is hard to lower my standard of living, so I try not to raise my standard of living and put that amount into investments.

I see on Twitter that there are salarymen who are accumulating 250,000 every month, and I'm not sure if I can go that far yet... I can go there if I cut back, but I don't want to put up with too much stress.

Anyway, I'm in a phase now where I need to increase my deposit power, or I'll go back to my parents' house. ....

- 150,000 yen monthly savings

By the way, I have the following savings settings. The top one is for the savings NISA setting.

If you are worried about stock selection, you can just buy all-country.

By the way, Leverage NASDAQ is the only negative in this list, although there is a problem with the start time. (LOL)

- For those who are confused about stock selection, the second all-country from the top for now

spot individual stock investments

When I receive a bonus or other large sum of money, I divide about 100,000-200,000 for fun and use the rest to buy individual stocks.

I buy companies that I personally want to support or am interested in.

The most recent stock I bought was JT, which is famous for its high dividend payout.

I was able to buy it right around the arrow, and within a month or two it announced a dividend increase and went up about 20% 🙂

1 million yen limit investment

Basically, I don't want to invest my assets in Japanese yen, so when my cash exceeds 1 million yen, I buy a mutual fund every month to bring my cash to about 1 million yen.

For reference, here are some investment-related literature I have read and recommend.

-

Stock Investment Notes (investment_April_24_2020_public.pptx

Tweet here by Yukie Yamaguchi, who is retiring early.

The book is a very comprehensive and well written book that could have cost 2,000~3,000 yen or more for a book and 5,000 yen or more for a notebook or something similar. U.S. Stocks

It is a very large book, but I think it is good to skim the first 65 pages or so.

By the way, if you read a little further, you will find that the book logically rejects dividend investment and special benefit investment. I don't invest mainly for dividends or special benefits either. -

Financial and economic education instructional materials for high schools published by the Financial Services Agency

If you are aware that your money literacy is low to begin with, you may want to read this first.

ppt : https://www.fsa.go.jp/news/r3/sonota/20220317/package.pptx

pdf : https://www.fsa.go.jp/news/r3/sonota/20220317/package.pdf

It can be found at the following sites

https://www.fsa.go.jp/news/r3/sonota/20220317/20220317.html -

A New Introduction to the Economy Written by a Former Goldman Sachs Interest Rate Trader

This is a book I read this year.

The book is a good introduction to money and monetary policy.

The concept of trade deficit and trade surplus

What exactly does negative GDP mean?

The Japanese national debt is the reason why some countries are going under, but is Japan safe?

The fundamental solution to the pension problem is not to save 20 million yen. -

The fundamental solution to the pension problem is not to put away 20 million yen. Keynesian Economics](https://amzn.to/3Se7Cy3)

I read this book when I was a university student, and I recommend it because even busy working people can read it in a few hours. However, it does not talk about practical investment, but rather about what wealth is in the world.

Aside.

I had no savings before I started working, and I started managing my assets after I changed jobs two and a half years ago. (I didn't accumulate any money at all during my previous job.)

I think I might reach 10 million in financial assets next year! I'm looking forward to seeing the status of my assets on Money Forward every month.

I hope to increase my deposit ability (salary) soon so that I can invest 250,000 a month or something like that.

What made me decide to write this article?

I started writing this article because I saw this note from a FF member and thought, "I've never written anything on my blog, even though I tweet about it.